When you’re trying to make Christmas special but money’s tight, buy now, pay later can look like a lifeline.

It promises no interest, no fees and the chance to spread the cost of presents, food and decorations.

But behind the bright adverts and easy payment buttons, there’s a real risk that can creep up fast when January comes around.

Get a free £10 bonus with Swagbucks

Earn a bit of extra money in your spare time with surveys, videos, and simple tasks you can do at home.

New users can get a £10 bonus when they sign up.

Get the £10 bonus

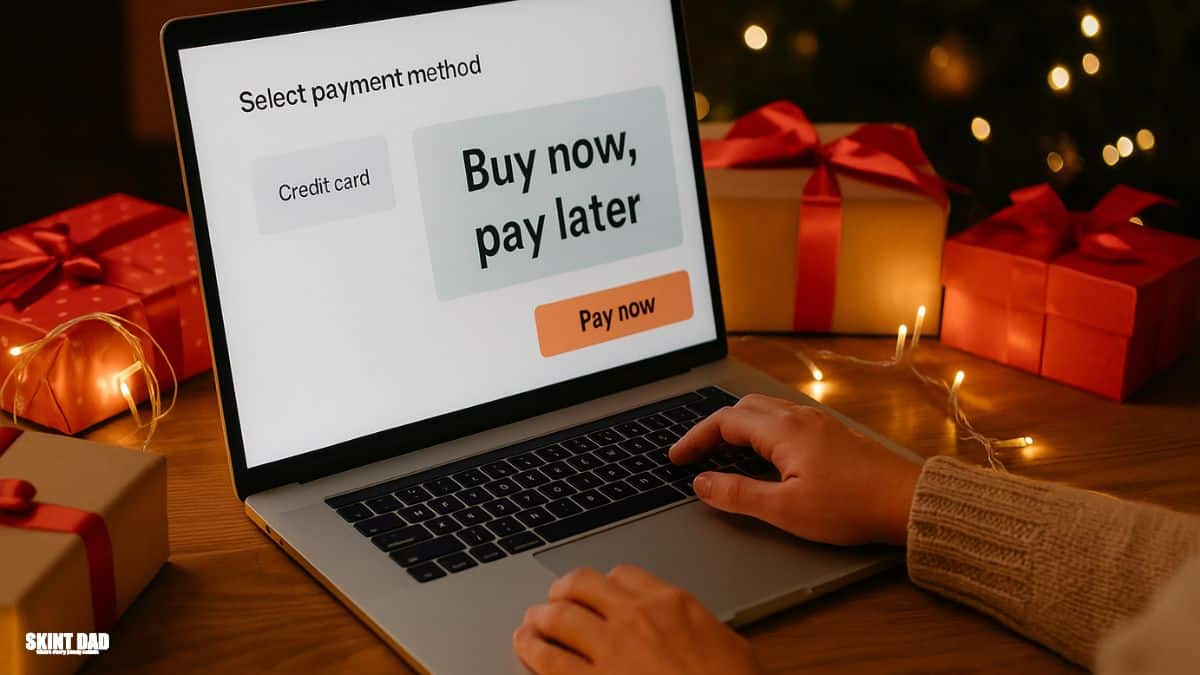

This year, millions of people across the UK will use services like Klarna, Clearpay and PayPal Pay in 3 to pay for gifts.

It’s tempting, especially when your budget’s already stretched and you just want to make the day feel magical.

But before you click that button at the checkout, it’s worth knowing how it really works, what could go wrong, and what you can do instead.

How buy now, pay later works

Buy now, pay later lets you take home your shopping now and split the payment over a few weeks or months.

Most of the big names claim to be “interest-free” as long as you pay on time. Some retailers offer even longer repayment plans with fixed monthly payments.

It sounds harmless enough. You get the items you need straight away, avoid a big one-off hit to your bank account, and pay it off bit by bit.

But there’s a catch. If you miss a payment or forget about a few different instalments, the money you owe can build up – and fast. Trust me, I naively got caught up like this years ago.

Late fees can apply, and while not every provider reports missed payments, more are starting to, which means it can affect your credit record and make it harder to get finance later on.

It also blurs the line between what you can afford and what you should afford. When there’s no upfront payment, it’s easy to spend more than you planned without really noticing.

Why it’s riskier at Christmas

There’s no time of year with more pressure to spend than Christmas. You want to give your kids a lovely day, treat your family, and keep up with everyone else.

Shops know this too, which is why buy now, pay later offers are everywhere right now.

The danger comes when those little “£20 here, £30 there” purchases start stacking up.

By the time the bills hit in January, along with higher energy costs and regular monthly expenses, your bank account can be under real strain.

Many people also take out more than one buy now, pay later plan across different retailers, which makes it harder to keep track of what’s due and when.

There’s also the emotional side. Paying later means you don’t feel the pain of spending straight away. You convince yourself that you’ll deal with it next month, but that’s exactly how the debt builds.

The hidden costs to watch out for

Even if the deal says no interest, that doesn’t mean it’s cost-free. Some companies charge late fees, others use debt collectors for missed payments, and the process can feel stressful if you fall behind.

Returns can cause problems, too. If you send something back but the refund takes a while, you might still have to make the next payment before the refund clears.

This can lead to confusion, overdraft charges, or missed instalments, which may leave a mark on your account.

And if you’re using a credit card to pay off your buy now, pay later plan, you could be paying interest twice, once to your card provider and again through missed BNPL payments.

And, you’re not actually paying it off; you’re just bouncing debt from one place to another.

It’s a slippery slope, especially when several small debts are sitting in the background.

Better ways to manage Christmas costs

If you want to spread the cost safely, there are still options.

Some supermarkets run Christmas savings clubs where you can pay in small amounts throughout the year and earn a bonus. It’s too late for this year, but it’s worth joining after Christmas for next time.

For now, think about setting up a small “Christmas pot” in your bank app. Monzo, Starling and Chase all let you set money aside automatically.

Even moving a few pounds a week helps you plan ahead without relying on credit.

Cashback apps and supermarket rewards can also help you cut costs on food, drink and gifts. Sites like TopCashback, Quidco and supermarket loyalty cards all add up when used regularly.

If you’re really struggling, look at local schemes and charities offering help with essentials this winter. They’re there to take some of the pressure off, not judge you for asking.

Skint Dad says:

Christmas shouldn’t come with a debt hangover. Companies make buy now, pay later sound harmless, but they’re not the ones checking your bank balance in January. Spend what you actually have, not what a lender says you can borrow. A cheaper Christmas you can afford is better than an expensive one that takes months to pay off.

Saved a few quid with our tips?

If Skint Dad has helped you spend less or feel more in control of your money, you can support the site with a small contribution.

- Side hustles and benefits in the UK: what you need to know - 8 January 2026

- Lloyds Bank switch deal: grab £250 plus Disney Plus for free - 6 January 2026

- Thinking of doing the Co-op freezer deal? Read this first - 6 January 2026